In a world that is flooded with information, our aim is to provide a high level – bird’s eye – view of the key factors and market determinants in the gas liquids sector, based on rigorous analysis and modelling

Meet the members of our leadership team

In a world that is flooded with information, our aim is to provide a high level – bird’s eye – view of the key factors and market determinants in the gas liquids sector, based on rigorous analysis and modelling

NGLStrategy, LLC’s methodology seeks to combine high-quality analytics with an understanding of how markets work, and companies behave

Fill in your details and our team will be in contact with you shortly

2025 | Houston

Ammonia is one of the fastest growing environmentally friendly products with a multitude of new applications and developments

Our experienced personnel can help your company to build up its NGL knowledge and understanding

Our analysis covers a wide range of NGL related topics

Our team has been involved in numerous NGL, Ammonia and Petchem Gases commercial projects for wide range of different clients.

Our wide range of regular reports provides an array of support and analysis to market participants

Our analysis covers a wide range of NGL related topics

We offers a wide range of services supporting your project teams

We are offering a full range of NGL/Petchem Gases/Ammonia consulting services

Our expertise covers the international space and the whole spectrum of the NGL/Ammonia chain

Tailor-made packages chosen by the client to give them maximum benefit and cost optimization

Our experienced personnel can help your company to build up its NGL knowledge and understanding

NGLStrategy LPG Market Seminar

10th April 2025 | Houston TX USA

In a world that is flooded with information, our aim is to provide a high level – bird’s eye – view of the key factors and market determinants in the gas liquids sector, based on rigorous analysis and modelling

Meet the members of our leadership team

In a world that is flooded with information, our aim is to provide a high level – bird’s eye – view of the key factors and market determinants in the gas liquids sector, based on rigorous analysis and modelling

NGLStrategy, LLC’s methodology seeks to combine high-quality analytics with an understanding of how markets work, and companies behave

Fill in your details and our team will be in contact with you shortly

2025 | Houston

Ammonia is one of the fastest growing environmentally friendly products with a multitude of new applications and developments

Our experienced personnel can help your company to build up its NGL knowledge and understanding

Our analysis covers a wide range of NGL related topics

Our team has been involved in numerous NGL, Ammonia and Petchem Gases commercial projects for wide range of different clients.

Our wide range of regular reports provides an array of support and analysis to market participants

Our analysis covers a wide range of NGL related topics

We offers a wide range of services supporting your project teams

We are offering a full range of NGL/Petchem Gases/Ammonia consulting services

Our expertise covers the international space and the whole spectrum of the NGL/Ammonia chain

Tailor-made packages chosen by the client to give them maximum benefit and cost optimization

Our experienced personnel can help your company to build up its NGL knowledge and understanding

NGLStrategy LPG Market Seminar

10th April 2025 | Houston TX USA

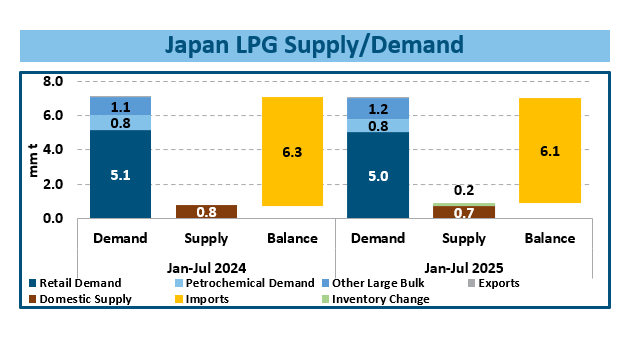

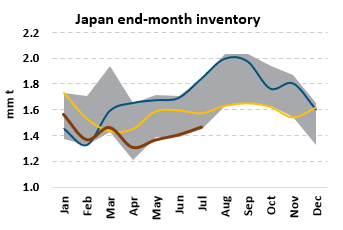

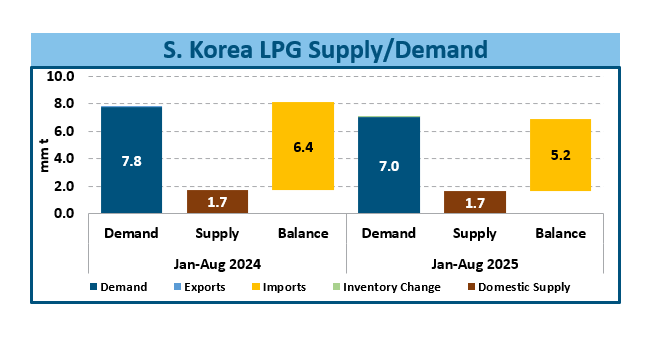

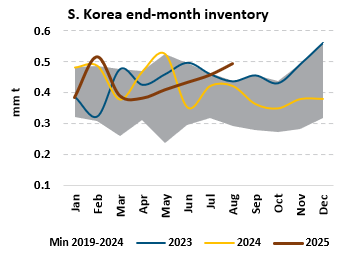

With the US-China trade tariffs being a dominant part of the LPG market in 2025, both Japan and S. Korea have been at the forefront as well as countries likely to “swap” US origin LPG cargoes for other non-US volume.